While the headlines chase whatever culture-war fire is burning that week, a genuinely consequential shift has been happening in fields, industrial parks, and old power-plant sites across the country: the United States is building, at real scale, an industry that barely existed five years ago — grid-scale battery storage.

These aren’t consumer gadgets. They’re shipping-container-sized battery units, install by the dozens or hundreds at a single site, that soak up electricity when it’s cheap or abundant — often midday solar — and release it when the grid needs it most: evening demand spikes, heat waves, or outages. They also perform quieter but critical jobs like frequency regulation and “black start,” the ability to re-energize a dead grid section after a blackout. This is the unglamorous infrastructure work that decides whether the lights stay on as the grid gets more renewable, more electrified, and more strained by things like data centers.

The scale is no longer small

For years, U.S. grid batteries were a niche built almost entirely on imported cells. That’s changed fast. By the close of 2025, American factories were producing roughly 70 GWh a year of finished grid storage systems — and that capacity is projected to climb to about 145 GWh/year by the end of 2026. For context, the entire U.S. grid-storage sector was closer to zero domestic cell-manufacturing capacity just a few years earlier.

The deployment side is moving just as fast. Combined U.S. battery storage deployments went from 6.5 GWh in 2022 to 14.7 GWh in 2023 to 31.4 GWh in 2024, and the pace has kept accelerating into 2026, with individual quarters now routinely topping 13 GWh from a single manufacturer.

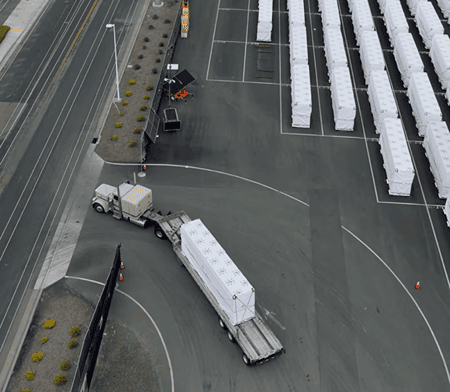

Tesla: the highest-profile player, not the only one

Tesla’s Megapack (pictured) and the newer Megablock get the most attention, and for good reason — the company is shipping at serious volume, deploying 13.5 GWh worldwide in Q2 2026 alone, and has broken its own deployment records repeatedly this year. Its newest hardware, the Megapack 3 and Megablock, pack more energy into a smaller footprint (roughly 5 MWh per Megapack 3 unit, up from 3.9 MWh in the prior generation) and are manufactured across plants in Fremont, Shanghai, and a new Houston-area facility built for 50 GWh/year of production.

But Tesla is one competitor in a much larger American buildout, not the whole story.

Fluence Energy — a joint venture born from Siemens and AES — is arguably the closest thing to a pure-play grid-storage leader in the U.S. It has built out manufacturing in Utah and Texas, hit its first profitable quarter with next-gen products like Gridstack Pro, and differentiates itself with software (its Mosaic platform automates bidding into wholesale power markets). The company has also emphasized domestically manufactured systems — U.S.-made cells, enclosures, inverters, and battery management systems — as onshoring and IRA compliance have become competitive advantages, not just talking points.

LG Energy Solution has quietly become a linchpin of the U.S. supply chain, even though it’s a Korean company operating heavily on American soil. Its Holland, Michigan LFP battery plant — the first large-scale U.S. facility making lithium iron phosphate cells specifically for grid storage — expanded to 25 GWh/year of capacity, and LG signed a $4.3 billion supply deal with Tesla to produce battery cells at a new Lansing, Michigan facility. It’s also still working with GM on separate battery production. In effect, LG has become one of Tesla’s own suppliers while building out parallel domestic capacity.

Samsung SDI and SK On round out the group of companies that, alongside Fluence, LG, and Tesla, make up the bulk of new U.S. grid-battery manufacturing capacity that didn’t exist domestically just a few years ago.

Why now

A few forces are converging:

- Policy: The federal Investment Tax Credit for storage projects held at 30% even as the consumer EV tax credit expired in late 2025 — a deliberate policy tilt favoring stationary storage over vehicle electrification.

- Grid strain: Rising electricity demand — driven in part by data centers and AI infrastructure — combined with more intermittent renewable generation on the grid has made storage less of a nice-to-have and more of a load-bearing necessity.

- Onshoring: Trade and national-security pressure around Chinese battery dominance (CATL, BYD) pushed Fluence, LG, and others to build domestic manufacturing specifically to produce IRA-compliant, U.S.-made systems.

- Falling costs: Lithium-ion prices have continued to decline, and newer hardware generations (Megapack 3, Fluence’s Smartstack, LG’s expanded LFP lines) are packing more energy density into smaller footprints, lowering the cost per megawatt-hour installed.

What it looks like on the ground

Real projects are already running, not just planned. Ontario’s Hagersville Battery Storage Park — Canada’s largest battery facility — came online in March 2026 using 92 Tesla Megapack units, providing 300 MW / 1,200 MWh of grid stabilization for Ontario’s system operator. In the U.S., similar projects are proliferating across Texas and California in particular, where labor and permitting have historically been bottlenecks that newer, factory-integrated products are specifically designed to reduce.

The bigger picture

None of this is as visually dramatic as a new EV or a rocket launch, and it’s easy to see why it gets less oxygen in the news cycle. But the underlying trend — the U.S. going from having almost no domestic grid-battery manufacturing to a projected 145 GWh/year of capacity in the span of a few years, spread across multiple competing American and America-based manufacturers — is a real, measurable shift in industrial capacity.

Every week, these strange white crates leave a high-security Tesla compound in Lathrop, California.

— Tony Seruga (@TonySeruga) July 5, 2026

They’re showing up near the Hoover Dam. At an Air Force base in Georgia. In the heart of New York City…

An estimated 4,000 of them are now spread across 48 locations in 14… pic.twitter.com/eDJO5vcWHr